Introduction:

Conforming loans play a pivotal role in the housing market, serving as a cornerstone for many homebuyers’ dreams. Whether you’re a first-time homebuyer or a seasoned investor, understanding the intricacies of conforming loans is essential. In this comprehensive guide, we’ll delve into the definition, characteristics, benefits, and potential challenges associated with conforming loans.

- Definition and Basics of Conforming Loans :

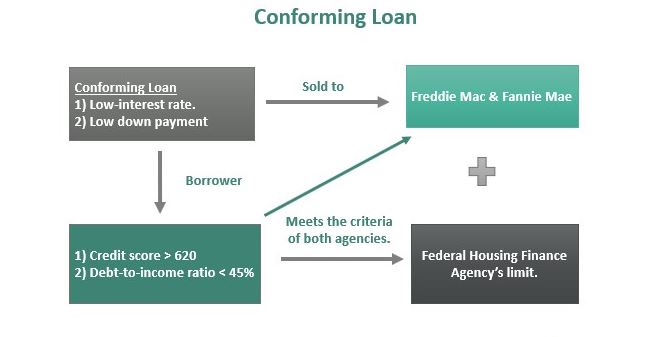

Conforming loans are a category of mortgage loans that adhere to specific criteria set by government-sponsored entities (GSEs) like Fannie Mae and Freddie Mac. These criteria typically include loan size limits, credit score requirements, and other eligibility criteria. The primary purpose of these guidelines is to maintain liquidity in the mortgage market and ensure that loans meet certain standards.

Conforming loans are distinct from non-conforming loans, commonly known as jumbo loans, which exceed the established limits. The loan limits are adjusted annually to reflect changes in the housing market and are influenced by factors such as regional home prices.

- Characteristics of Conforming Loans :

- Loan Limits and Regional Variances:

Conforming loans are subject to specific loan limits, which vary by location. In high-cost areas, these limits are higher to accommodate the elevated property values. Understanding the loan limits is crucial for both lenders and borrowers, as exceeding these limits categorizes the loan as non-conforming.

- Credit Score Requirements:

Conforming loans often require a reasonable credit score, although the exact threshold may vary. A higher credit score generally improves the borrower’s chances of securing a more favorable interest rate. However, conforming loans may still be accessible to borrowers with moderate credit scores.

- Down Payment and Debt-to-Income Ratio:

The down payment and debt-to-income ratio are key factors in conforming loan approval. While it’s possible to secure a conforming loan with a lower down payment compared to non-conforming loans, a higher down payment often results in better terms. Lenders also assess the borrower’s debt-to-income ratio to gauge their ability to manage monthly payments.

- Interest Rates:

Conforming loans typically offer lower interest rates compared to non-conforming loans. This is partly due to the perceived lower risk associated with conforming loans, as they adhere to standardized criteria set by GSEs.

III. Benefits of Conforming Loans :

- Lower Interest Rates:

One of the primary advantages of conforming loans is the potential for lower interest rates. This can result in significant long-term savings for borrowers, making homeownership more affordable.

- Wider Accessibility:

Conforming loans are designed to be accessible to a broader range of borrowers. With reasonable credit score requirements and flexible down payment options, these loans cater to both first-time homebuyers and repeat buyers.

- Secondary Market Liquidity:

Conforming loans contribute to the liquidity of the secondary mortgage market. Once originated, these loans can be sold to investors, freeing up capital for lenders to issue new loans.

- Standardized Process:

The standardized criteria for conforming loans streamline the mortgage application and approval process. Borrowers benefit from a more transparent and predictable experience.

- Potential Challenges with Conforming Loans:

- Strict Eligibility Criteria:

While conforming loans offer accessibility, the rigid eligibility criteria may pose challenges for certain borrowers. Those with unique financial situations or credit issues may find it more difficult to qualify.

- Geographic Limitations:

The regional variations in loan limits may present challenges for borrowers in high-cost areas. In such regions, borrowers might find themselves constrained by lower loan limits, necessitating the consideration of alternative financing options.

- Property Type Restrictions:

Conforming loans may have restrictions on the type of property financed. Certain property types, such as investment properties or vacation homes, may not qualify for conforming loan programs.

In conclusion, conforming loans are a cornerstone of the mortgage market, offering benefits such as lower interest rates, accessibility, and a standardized process. However, potential challenges exist, including strict eligibility criteria and geographic limitations. Aspiring homeowners and real estate investors must carefully weigh the pros and cons of conforming loans to make informed decisions that align with their financial goals and circumstances. Understanding the dynamics of conforming loans is a crucial step towards navigating the complex landscape of mortgage financing.

In the vast landscape of real estate and mortgage financing, one term that frequently emerges is “conforming loans.” For aspiring homebuyers or those looking to refinance, comprehending the intricacies of conforming loans is crucial. This comprehensive guide aims to shed light on what conforming loans are, how they differ from other types of mortgages, and their significance in the housing market.

- The Basics of Conforming Loans

- Definition

Conforming loans are a category of mortgage loans that adhere to specific guidelines set by government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac. These guidelines encompass various criteria, including loan amount, borrower creditworthiness, and property type. In essence, conforming loans “conform” to the standards established by these entities.

- Criteria for Conformity

- Loan Limits: Conforming loans must fall within the predefined loan limits set by the GSEs. These limits vary by geographic location and are subject to periodic adjustments based on changes in the housing market.

- Creditworthiness: Borrowers seeking conforming loans are typically required to have a reasonably good credit score. The specific score threshold may vary, but a solid credit history is generally a prerequisite.

- Down Payment: While conforming loans may offer more favorable down payment terms compared to some other mortgage types, borrowers are still required to contribute a certain percentage of the home’s purchase price.

- Debt-to-Income Ratio: Lenders evaluate borrowers’ debt-to-income ratio to ensure they have the financial capacity to repay the loan. Conforming loans often have specific requirements regarding this ratio.

- Conforming Loans vs. Non-Conforming Loans

Understanding conforming loans becomes more apparent when juxtaposed with non-conforming loans, often referred to as jumbo loans.

- Loan Amount

The primary distinction between these two categories lies in the loan amount. Conforming loans adhere to the established limits, whereas non-conforming loans surpass these limits. Jumbo loans, a common type of non-conforming loan, are sought when financing high-value properties that exceed the conforming loan limits.

- Risk and Interest Rates

Due to their adherence to GSE guidelines, conforming loans are generally perceived as lower risk by lenders. As a result, borrowers may benefit from lower interest rates compared to non-conforming loans. Non-conforming loans, especially jumbo loans, carry a higher risk for lenders, often translating into higher interest rates for borrowers.

- Market Accessibility

Conforming loans cater to a broader segment of the housing market, providing more accessibility to a range of borrowers. Non-conforming loans, being more specialized, may be subject to stricter approval criteria and may be less accessible to some homebuyers.

III. The Role of Fannie Mae and Freddie Mac

Fannie Mae and Freddie Mac, two of the most prominent GSEs, play a pivotal role in the conforming loan landscape.

- Secondary Mortgage Market

Fannie Mae and Freddie Mac do not directly issue loans to borrowers. Instead, they purchase conforming loans from lenders on the secondary mortgage market. This process allows lenders to replenish their funds and continue originating new loans, promoting liquidity in the mortgage market.

- Standardization and Guidelines

These entities establish and enforce guidelines that lenders must follow when underwriting conforming loans. This standardization ensures a level of consistency in the mortgage market, contributing to its stability.

- Advantages and Considerations for Borrowers

- Lower Interest Rates

One of the most notable advantages of conforming loans is the potential for lower interest rates. Lenders view these loans as less risky, translating into more favorable terms for borrowers.

- Easier Approval Process

Conforming loans often undergo a more streamlined approval process compared to non-conforming loans. This can be particularly advantageous for borrowers seeking a quicker and more straightforward mortgage approval.

- Market Accessibility

Conforming loans open doors for a broader range of homebuyers, promoting inclusivity in the real estate market. This inclusivity is essential for fostering a healthy and dynamic housing environment.

- Potential Limitations

While conforming loans offer numerous advantages, there are limitations to consider. Borrowers whose financing needs surpass the conforming loan limits may need to explore alternative options, such as non-conforming or jumbo loans.

In the intricate realm of mortgage financing, conforming loans stand as a cornerstone, providing stability and accessibility to a diverse array of homebuyers. Understanding the nuances of conforming loans empowers individuals to make informed decisions as they navigate the path to homeownership or explore refinancing opportunities. As the real estate landscape evolves, so too will the role and significance of conforming loans, ensuring their continued impact on the housing market.

In the dynamic landscape of business financing, entrepreneurs are constantly seeking innovative solutions to fuel their growth. Royalty financing loans have emerged as a unique and flexible option for businesses looking to secure capital without traditional debt or equity structures. This comprehensive guide will explore the intricacies of royalty financing loans, shedding light on what they are, how they work, their advantages, potential challenges, and real-world applications.

- Understanding Royalty Financing Loans :

Royalty financing loans, also known as revenue-based financing or royalty-based financing, represent a distinct approach to business funding. In this model, a company secures capital by promising investors a percentage of its future revenues over a specified period. Unlike traditional loans, royalty financing doesn’t involve fixed interest rates or ownership dilution. Instead, investors become entitled to a share of the company’s top-line revenue.

- Mechanics of Royalty Financing Loans :

- Agreement Structure:

Royalty financing agreements are structured around a set percentage of gross revenues. The terms can vary, but they often include a predetermined cap or a total return limit for investors.

- Repayment Structure:

As the business generates revenue, a portion is allocated to repay the investor until the agreed-upon amount is fulfilled. This dynamic structure aligns the interests of both parties, fostering a symbiotic relationship.

- Duration of Agreement:

The duration of royalty financing agreements varies and is typically determined during negotiations. It may span a fixed period, a specific revenue multiple, or until a predetermined cap is reached.

III. Advantages of Royalty Financing Loans :

- No Equity Dilution:

Unlike equity financing, royalty financing allows businesses to secure capital without relinquishing ownership or control. Entrepreneurs can benefit from the infusion of funds while retaining the strategic direction of their companies.

- Flexible Repayment:

The repayment structure based on a percentage of revenue offers flexibility. In slower periods, when revenues may be lower, the repayment amount adjusts accordingly. This feature mitigates the financial strain during challenging business cycles.

- Alignment of Interests:

Royalty financing aligns the interests of investors and business owners. Investors succeed when the business performs well, creating a shared goal of maximizing revenue and profitability.

- Access to Growth Capital:

For companies with promising revenue streams but limited assets, royalty financing provides access to growth capital. This can be particularly advantageous for businesses in sectors such as technology, where traditional collateral may be scarce.

- Challenges of Royalty Financing Loans :

- Potential Cost:

While royalty financing offers flexibility, it may come at a higher cost compared to traditional loans. The effective interest rate, when calculated over time, might be higher, reflecting the risk undertaken by investors.

- Limited Applicability:

Royalty financing may not suit all business models. Companies in industries with erratic revenue streams or extended gestation periods before profitability may find it challenging to attract royalty financing investors.

- Complex Negotiations:

Crafting a royalty financing agreement can be complex. Negotiating the percentage of revenue, duration, and any caps requires a thorough understanding of the business and its future prospects. Legal and financial expertise is crucial in this process.

- Real-World Applications :

- Startups and Emerging Businesses:

Royalty financing is increasingly popular among startups and emerging businesses with promising revenue projections. It provides a non-dilutive funding option, allowing these companies to scale without sacrificing ownership.

- Technology and Innovation:

In the fast-paced world of technology, where traditional metrics may not fully capture a company’s value, royalty financing becomes an attractive option. Tech companies with substantial intellectual property and potential future revenues can leverage this form of financing.

- Seasonal Businesses:

Seasonal businesses, such as those in tourism or retail, can benefit from the flexibility of royalty financing. Repayments tied to revenue align with the seasonal nature of their cash flows.

Royalty financing loans represent a paradigm shift in business financing, offering an alternative to traditional debt and equity structures. With their flexibility, alignment of interests, and applicability to various business models, these loans have the potential to unlock growth for a wide range of companies. However, entrepreneurs must carefully assess the cost, negotiate terms diligently, and consider the compatibility of royalty financing with their business models. As the financial landscape evolves, royalty financing stands as a compelling option for those seeking innovative and tailored approaches to fuel their ventures.